Capturing Market Share in Menswear

A hot topic for Lululemon (“LULU”) has been capturing market share in menswear, especially as the sub-industry develops among brands that have historically been associated with a focus on female consumers. This is a growing category with a lot of potential - the company frequently references their outstanding goal to double men’s revenues by 2023 (vs. 2019 levels)*.

For a brand like LULU that was built on addressing the needs of female consumers, there are two key questions to answer:

- Do LULU’s products meet the needs of male consumers?

- Will LULU be able to convince male consumers to buy their products when the association in many consumers’ minds is that LULU is a brand that makes products for female consumers?

Does LULU have products that men love and want to buy?

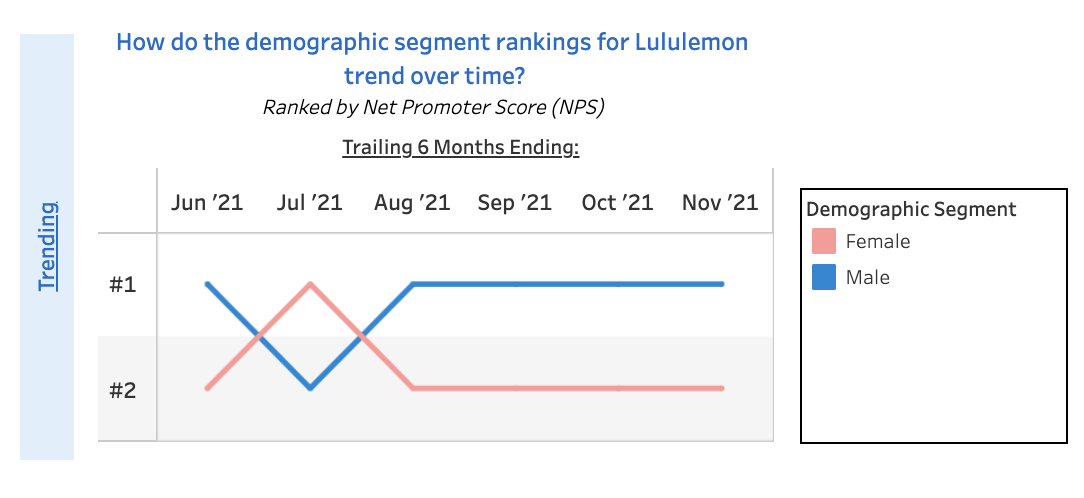

HundredX Demographic Segment Rankings (Gender) - Trailing 6 Months Trend

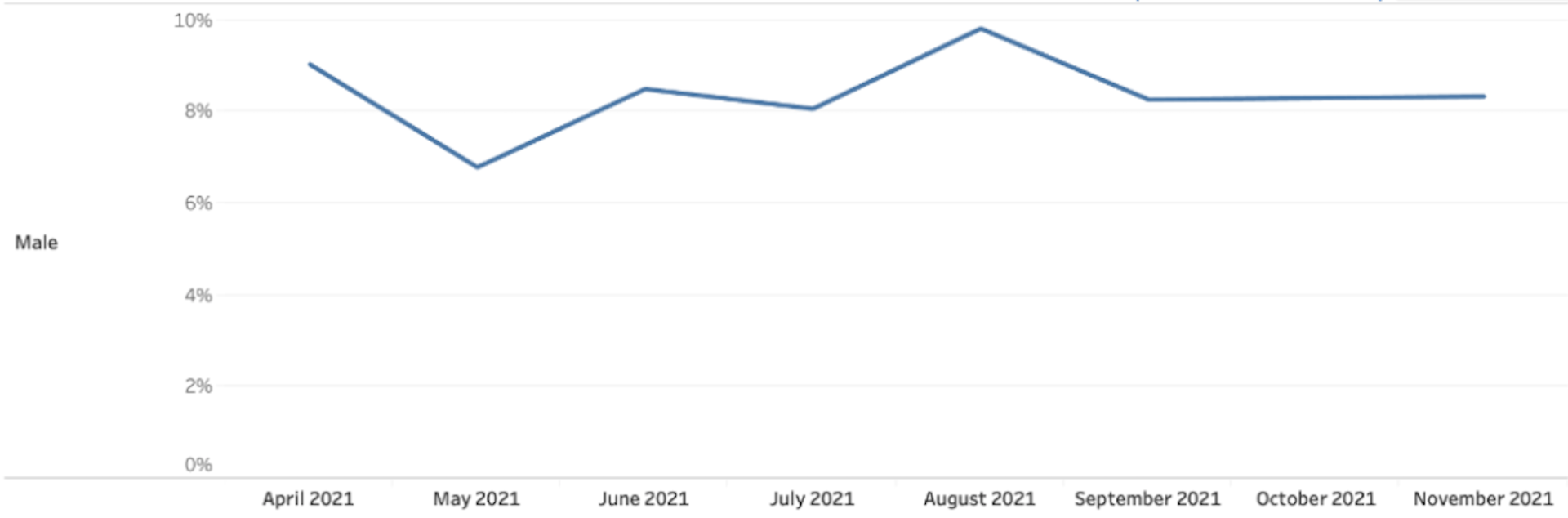

HundredX Net Positive Future Purchase Intent Rankings by Gender - Trailing 6 Months Trend

HundredX data for LULU shows that male customers of the company love their products. So much so that starting in August 2021, NPS for male customers has ranked above NPS for female customers. In addition, the strong NPS from male consumers has translated into a consistently strong desire to purchase more from the company in the next 12 months.

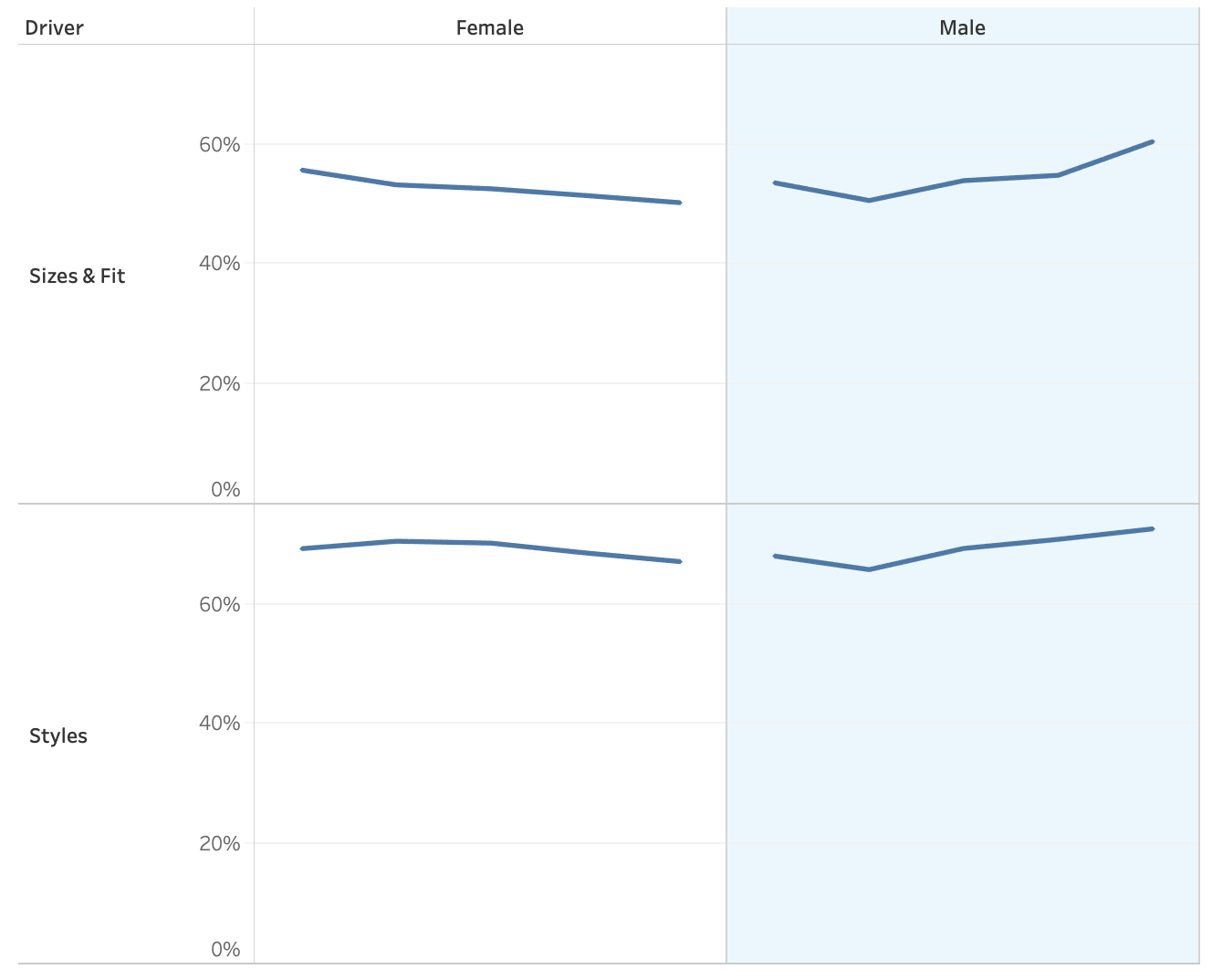

HundredX Driver Trends by Gender - Trailing 3 Months Trend

In a review of drivers for LULU by gender, the company’s core value proposition of high quality, outstanding fit, and appealing styles appears very consistent between male and female customers. Similarly, both male and female customers knock LULU for its prices. However, while the directional trends for Sizes & Fit and Styles are relatively stable for female customers, the same drivers for male customers show strong improvement over recent months. These trends suggest that LULU is finding its groove making clothing that male consumers like.

Will LULU continue to convince more and more male consumers to buy its clothing?

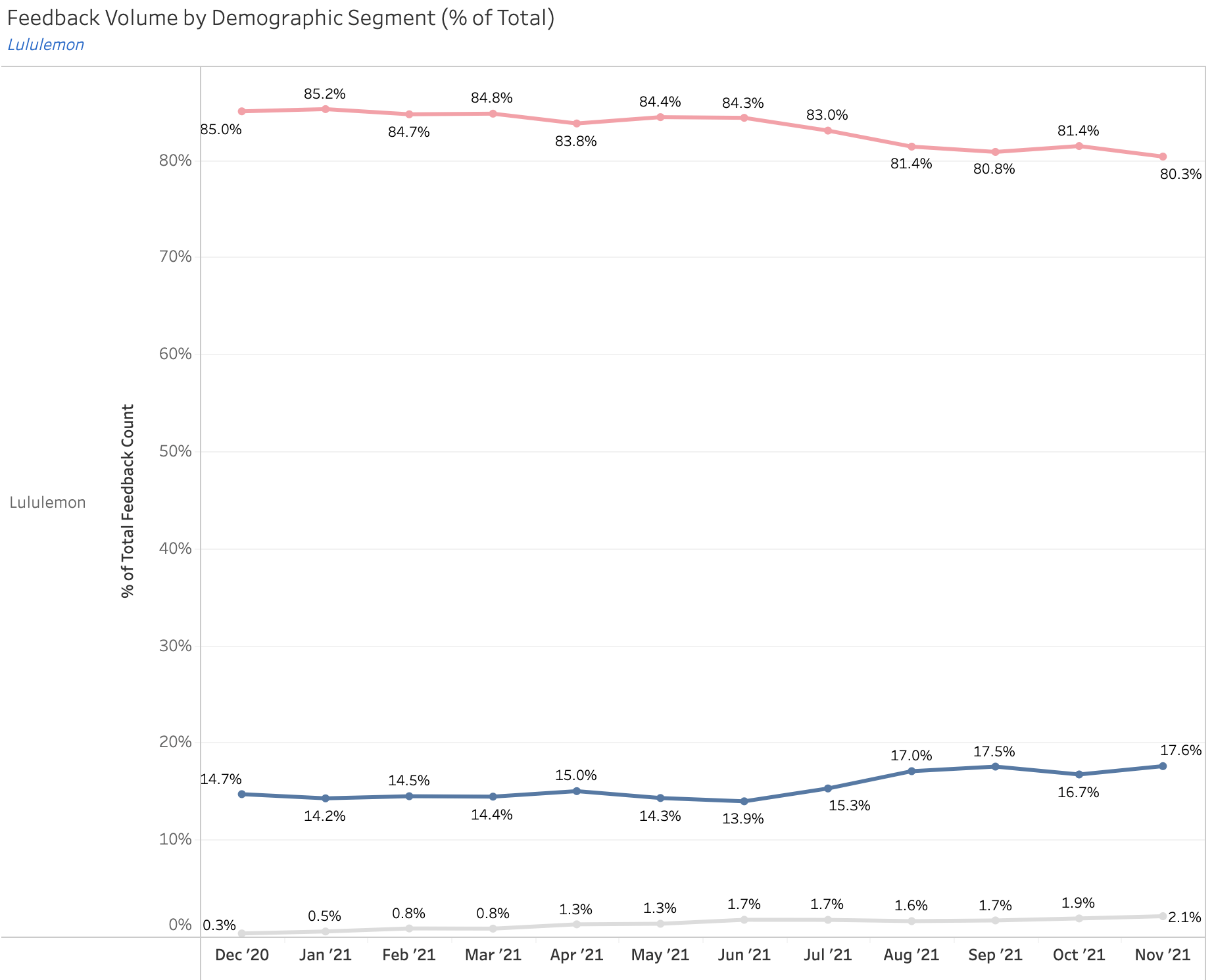

HundredX Feedback Volume by Gender for LULU, Trailing 6 Month Trend

On a trailing 6 month basis for the period ending in November 2021, 80.3% of HundredX feedback for LULU comes from female customers while 17.6% comes from male customers. The disparity indicates that LULU is still strongly viewed as a brand for female consumers first and male consumers second. However, the trend shows the company picking up steam with male consumers, with particular acceleration since early summer 2021. These trends would suggest that the company’s plans to engage new male customers is starting to gain traction with consumers.

*Selection of LULU management references to growth goals in male consumer segment:

- CNBC article from April 2019 discussing Lululemon’s goals with male consumers: Lululemon CEO: 'We have very low brand awareness with men,' but that business will double by 2023

- Lululemon Athletica Inc. (LULU “Power of Three” Strategic Plan - Apr 2019

- Lululemon Athletica Inc. (LULU) Q3 2021 Earnings Call Transcript

This analysis is based on HundredX's proprietary data, developed from consumer feedback collected through the

HundredX Causes Program. Nothing in the HundredX data constitutes professional or investment advice on the part of HundredX.

Strategy Made Smarter

HundredX works with a variety of companies and their investors to answer some of the most important strategy questions in business:

- Where are customers "migrating"?

- What are they saying they will use more of in the next 12 months?

- What are the key drivers of their purchase decisions and financial outcomes?

Current clients see immediate benefits across multiple areas including strategy, finance, operations, pricing, investing, and marketing.

Our insights enable business leaders to define and identify specific drivers and decisions enabling them to grow their market share.

Please contact our team to learn more about which businesses across 75 industries are best positioned with customers and the decisions you can make to grow your brand’s market share.

Share This Article