At a time when many companies are worried about consumer’s wallets and the outlook for the US economy remains mixed and hotly debated, we take a close look at one of the key factors in that debate – prices. HundredX has examined the movement in consumer price sentiment, leveraging our proprietary data. Reviewing over 7 million pieces of feedback since July 2021, spanning over 80 industries, and nearly 3,000 companies, we find:

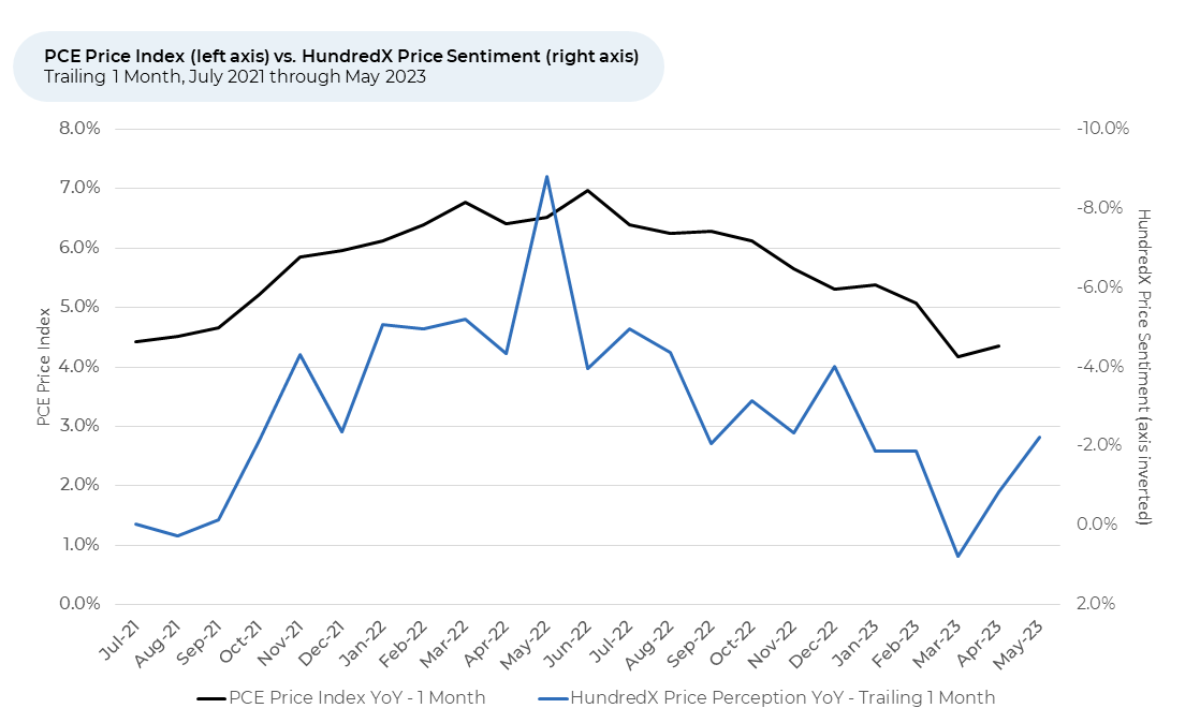

- Price sentiment fell for the second consecutive month in May. We have found changes in HundredX’s Price sentiment¹,² index typically inversely correlate with movement in the Personal Consumption Expenditures (PCE) Price levels (i.e. inflation) reported by the US government.

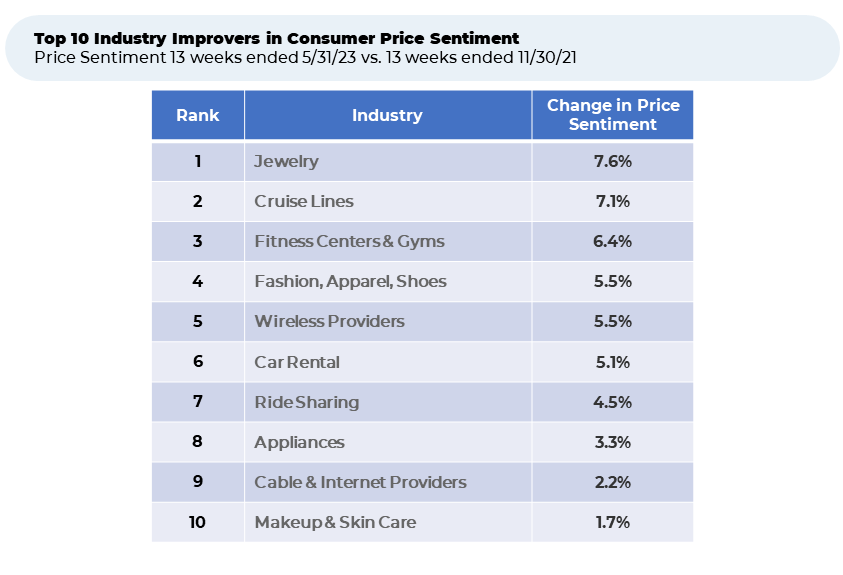

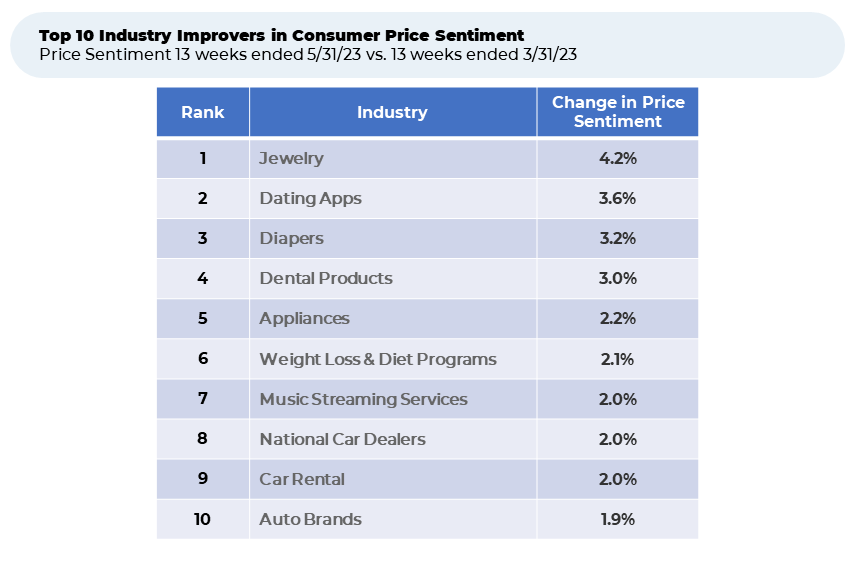

- In the last two months (when aggregate sentiment has fallen), sectors selling expensive items, such as jewelry, cars, and appliances, were among the top 10 improvers in Price sentiment.

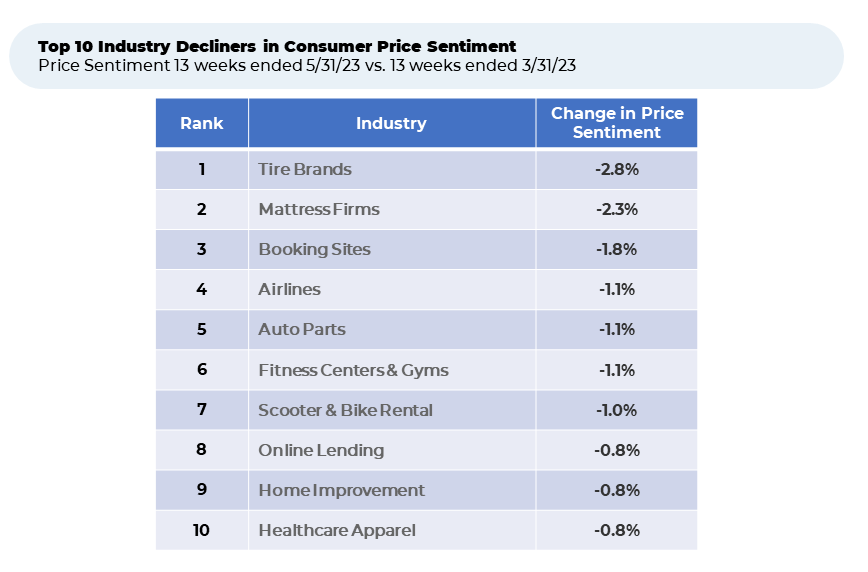

- Over the same two months, travel and transportation, home-related and car parts industries accounted for most of the top 10 decliners in Price sentiment.

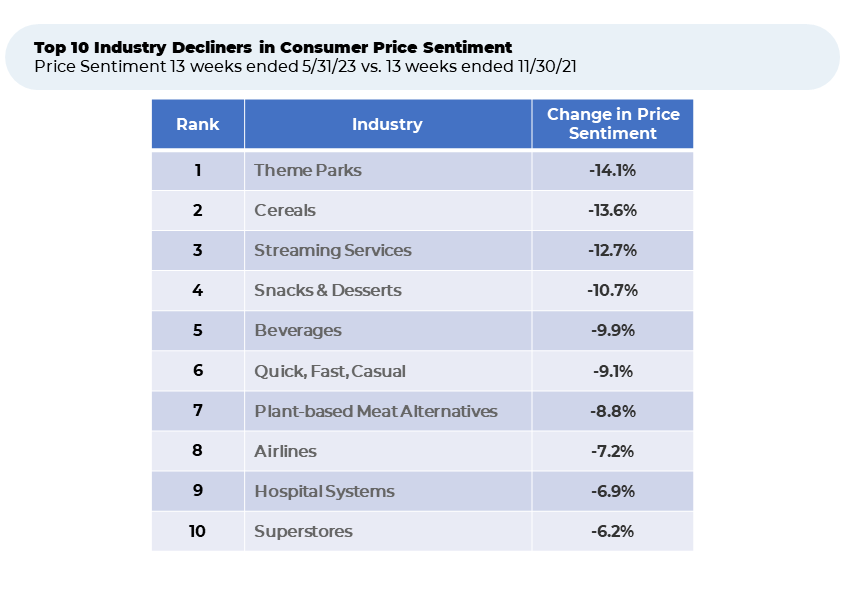

- Taking a look back over the most recent period of record inflation, food-related sectors accounted for 5 of the top 10 declines in Price Sentiment in May 2023 vs. 18 months before.

- Industries heavily affected by the pandemic (such as cruises and fitness centers), some discretionary items and utilities like cell phones and cable saw the biggest Price sentiment improvements the last 18 months.

HundredX sees movement in Price Sentiment before inflation gets reported

In 2021, inflation began to surge across the US domestic economy as businesses dealt with supply and labor challenges and periods of loosening activity restrictions by the government in dealing with the COVID-19 pandemic. According to feedback from the “Crowd” of millions of real customers, Aggregate Price Sentiment for all the industries HundredX follows weakened from July 2021 to May 2022, where it finally troughed.

Over much of the past year there had been a steady improvement in Price sentiment through March 2023, before it declined modestly in April and again in May. This trend inversely aligns with movement in the PCE Price index, which rose from July 2021 to a June 2022 peak before moderating most of the last year. The May 2023 PCE Price Index reading will be released June 30.

The recent decline in price sentiment observed in the past two months indicates there are signs of consumer discontent resurfacing, particularly as economic growth decelerated in 1Q 2023 and inflation remains above historical levels. We take a closer look at the industries that have seen sentiment improve and decline most.

Looking closer at the HundredX data, about two-thirds of the industries we follow saw a decline in price sentiment from November 2021 through May 2023, while only one-third experienced an improvement. By contrast, about two-thirds of followed industries saw improvements in the last two months while one-third saw declines (most of them modest).

Vehicle maintenance and summer travel causing recent declines in Price Sentiment

While there are a range of industries in the top 10 for recent declines in Price Sentiment, a handful were particularly interesting to us. Tire Brands in particular sticks out as the top decliner, along with Auto Parts at #5. As automotive prices continue to remain high and interest rates rise,

consumers are opting to hold onto their cars for longer. This trend could potentially result in increased vehicle repairs and the purchase of new tires, thereby driving up the prices of items necessary for maintaining their cars and frustrating consumers.

It comes as no complete surprise that booking sites and airlines rank among the top decliners in price sentiment. Airline prices are up versus the prior month in May, though they are down meaningfully versus last year. Booking sites covered by HundredX includes comprehensive sites like Expedia.com as well as vacation rental sites like Airbnb and Vrbo. Hotels also saw prices up versus the prior month to record levels in May. Both are up as usual headed into the summer season, as consumers' desire to vacation rises. One recent flier shared with HundredX in May, “The prices have just gone up so much that it is more than the hotel costs.” Another shared “Pricing increasing faster than inflation”, while a recent vacation rental customer complained, “The fees can be high for just 1-2 nights. The prices overall have increased too much.”

Food-related industries hit hard in 2022 continue to decline

Food-related industries were hit hardest by inflation during 2022, leading them to be amongst the worst price sentiment decliners in the eyes of the consumer over the last 18 months. Cereals, Snacks & Desserts, Beverages, Quick/Fast/Casual, and Plant-based Meat Alternatives all are among the top 10, down 9%-14%. While the decline in sentiment was primarily concentrated in 2022, they were all down further in 2023.

Many industries beat up by the pandemic saw strong price sentiment bounce back

After being severely impacted by the pandemic, certain industries have witnessed a promising rebound in Price sentiment compared to 18 months ago. Cruise Lines, Fitness Centers & Gyms, Car Rental, and Ride Sharing are displaying encouraging signs of recovery, with all of them among the top 10 movers in Price Sentiment.

However, some industries impacted by the pandemic continue to struggle, as Airlines (-7%) & Movie Theaters (-6%) rank among the worst in change of Price Sentiment over the last 18 months.

Big ticket items showing improvement in Price Sentiment in Recent Months

Despite high inflation, sectors selling big-ticket items such as jewelry, cars and appliances have seen an improvement in price sentiment. This raises questions about whether wealthier customers buying these products are simply getting accustomed to higher prices, if rising wages are offsetting the negative sentiment caused by inflation or the businesses may be starting to reduce prices (but haven’t reported financial results yet). We will continue to watch for evidence to answer these important questions in the coming weeks.

- All metrics presented, including Net Positive Percent / Sentiment are presented on a trailing three-month basis unless otherwise noted.

- HundredX measures sentiment towards a driver of customer satisfaction as Net Positive Percent (NPP), which is the percentage of customers who view a factor as a positive (reason they liked the products, people, or experiences) minus the percentage who see the same factor as a negative.

Strategy Made Smarter

HundredX works with a variety of companies and their investors to answer some of the most important strategy questions in business:

- Where are customers "migrating"?

- What are they saying they will use more of in the next 12 months?

- What are the key drivers of their purchase decisions and financial outcomes?

Current clients see immediate benefits across multiple areas including strategy, finance, operations, pricing, investing, and marketing.

Our insights enable business leaders to define and identify specific drivers and decisions enabling them to grow their market share.

Please contact our team to learn more about which businesses across 75 industries are best positioned with customers and the decisions you can make to grow your brand’s market share.

####

HundredX is a mission-based data and insights provider. HundredX does not make investment recommendations. However, we believe in the wisdom of the crowd to inform the outlook for businesses and industries. For more info on specific drivers of customer satisfaction, other companies within 75+ other industries we cover, or if you'd like to learn more about using Data for Good, please reach out: https://hundredx.com/contact.

Share This Article